By Johar Tarabeih

This article revisits a section of my Masters Thesis, where I used causal inference methods to analyze the impact of the European Payment Services Directive 2 (PSD2) –will continue updating for clarity and brevity.

***Important*** For relevant citations, references, and attributions, as well as more in-depth exploration on regional determinants of digital banking adoption, please reference the original paper:

Motivation

The digital transformation of Europe has accelerated sharply over the past decade, shifting internet-based services from optional tools to structural necessities. Household internet access in the European Union increased from roughly 80 percent in 2014 to over 94 percent by 2024, reflecting not only expanded connectivity but a reorganization of how public services, labor markets, and personal finances operate. Digital technologies now condition access to the state, employment, and essential services, making digital infrastructure and literacy prerequisites for full participation.

This transition has been uneven. Despite widespread internet access, persistent gaps remain in digital usage and skills, commonly referred to as the digital divide. These disparities are closely tied to structural factors such as education, income, age, and geography, raising concerns about the exclusion of rural populations, lower-income households, and older adults. In response, the European Commission’s Digital Decade initiative set targets for connectivity, skills, and public service digitization to promote inclusive digital development amid rapid technological change.

Digital banking provides a clear illustration of this gap. While over 90 percent of individuals report using the internet, only about 64 percent use digital banking services. This divergence persists despite the clear advantages of digital banking, including continuous access, improved financial oversight, and increased competition among institutions. The gap suggests that adoption is not driven by access alone, but by how individuals and regions evaluate and internalize digital technologies.

Foundations

Understanding why individuals adopt digital banking requires looking beyond access and toward how technologies are evaluated. The Technology Acceptance Model, introduced by Davis (1989) and extended by Venkatesh and Davis (1996), provides a parsimonious framework for doing so. Built on the Theory of Reasoned Action, TAM models adoption as a function of beliefs that shape behavioral intention, rather than as a direct response to availability or mandate.

At its core, TAM identifies two latent determinants of adoption. Perceived Usefulness (PU) captures whether users believe a technology improves outcomes or performance. Perceived Ease of Use (PEoU) reflects the cognitive effort required to use it. These perceptions mediate the influence of external conditions such as institutions, regulation, skills, and infrastructure on actual usage. Empirically, adoption decisions are driven primarily by perceived usefulness, with ease of use playing a secondary and often indirect role by reinforcing perceived value.

This structure makes TAM especially relevant for digital banking. Banking adoption is not binary access but a valuation problem. Individuals with internet access still choose whether the expected benefits of digital banking exceed perceived costs. Non-adoption therefore reflects suppressed perceived usefulness, elevated perceived risk, or both. A large empirical literature applying TAM to digital banking consistently finds that higher perceived usefulness strongly predicts adoption, while perceived ease of use matters mainly insofar as it shapes usefulness.

A central extension of TAM in the financial context concerns trust and perceived risk. Banking inherently requires confidence in institutions to safeguard assets and personal data. Digitization introduces additional risks related to fraud, data breaches, and platform security. The literature shows that higher perceived risk reduces adoption by lowering perceived usefulness, while stronger trust in digital platforms increases it. These effects are robust across countries and income levels and help explain why adoption lags even when digital infrastructure is in place.

This framework provides a clear lens for policy analysis. If adoption depends on perceived usefulness, then regulatory interventions that improve security, standardize protections, or enhance functionality should increase adoption by shifting beliefs rather than access. The Second Payment Services Directive (PSD2) fits this mechanism closely. By strengthening consumer protections, mandating secure authentication, and promoting competition and interoperability, PSD2 plausibly raised the perceived usefulness of digital banking. Its staggered implementation across EU countries therefore offers a natural setting to test whether increasing perceived usefulness translates into higher adoption.

This logic motivates the use of a difference in differences framework. Rather than asking whether digital banking is popular, the analysis asks whether a policy induced shift in perceived usefulness reduced the share of internet users who abstain from digital banking. In doing so, it operationalizes TAM at scale and links behavioral theory directly to institutional change.

Policy Background

The revised Payment Services Directive (PSD2) was adopted by the European Parliament on November 25, 2015, replacing the original 2007 directive. The revision responded to the rapid expansion of digital payments and fintech platforms, alongside growing consumer concerns over security, fraud, and regulatory gaps in online financial services.

PSD2 pursued four primary objectives. First, it aimed to further integrate digital payment systems across the EU. Second, it sought to increase competition by opening payment markets to new providers. Third, it strengthened the safety and security of digital payment systems. Fourth, it enhanced consumer and business protections at the European level. These objectives were operationalized through binding regulatory standards, including Strong Customer Authentication requirements, mandatory incident reporting by financial institutions, and expanded refund and liability protections for consumers.

Member states were required to transpose PSD2 into national law by January 13, 2018, but implementation occurred at different points across countries between 2017 and 2020. This staggered rollout creates meaningful variation in the timing of exposure to enhanced digital payment protections.

The relevance of PSD2 to the Technology Acceptance Model is direct. Banking adoption fundamentally depends on trust in an institution’s ability to safeguard financial assets. In this sense, security is inseparable from perceived usefulness. If a financial system cannot guarantee safety, its usefulness is inherently diminished. By strengthening authentication, oversight, and consumer protections, PSD2 plausibly increased the perceived usefulness of digital banking for existing internet users.

If perceived usefulness is a key driver of adoption, as TAM predicts, then the implementation of PSD2 should lead to increased digital banking adoption among internet users. Empirically, this implies a reduction in the Digital Banking Differential following implementation. Testing this prediction provides a policy-based evaluation of TAM’s core mechanism and motivates the empirical analysis of Hypothesis 1.

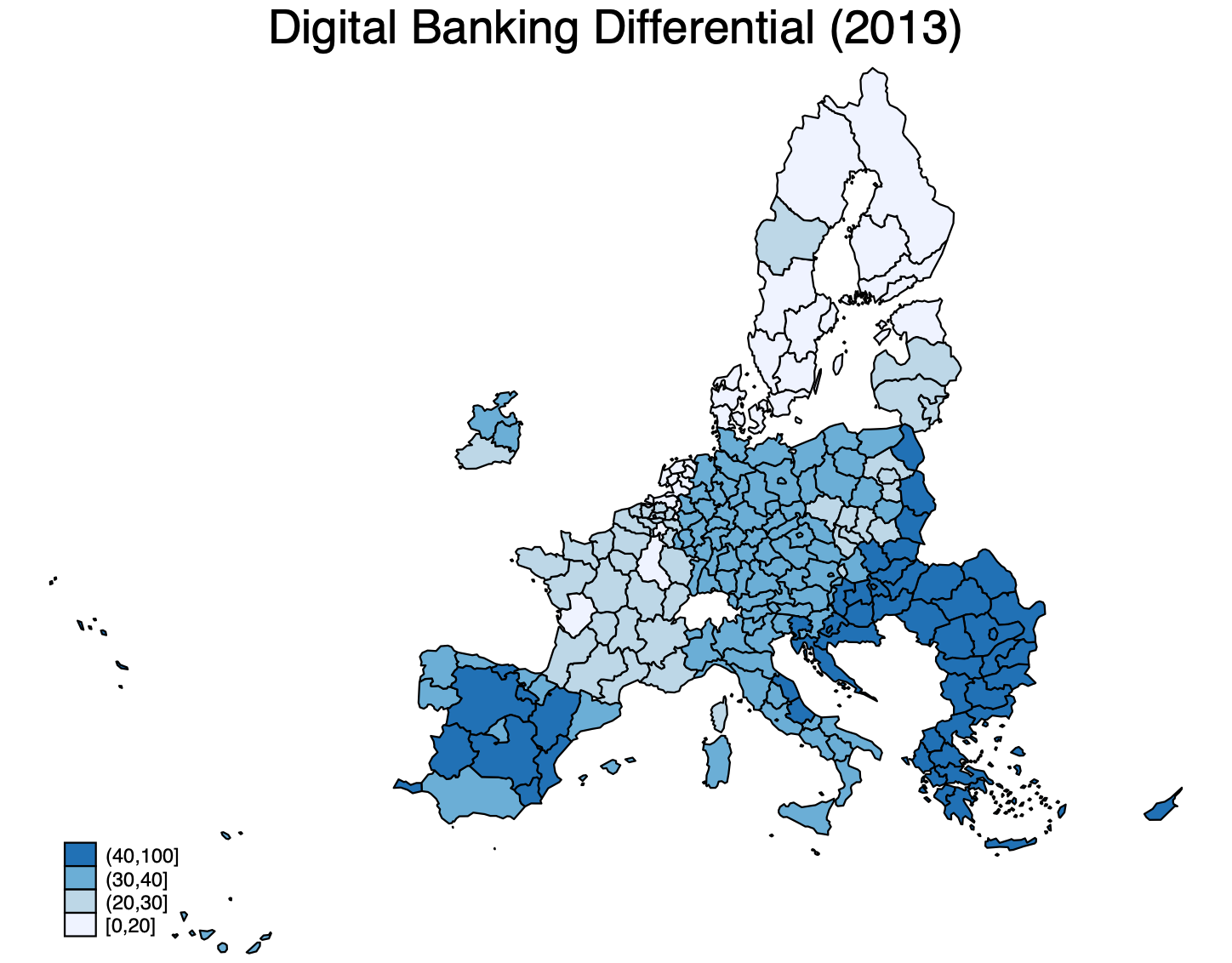

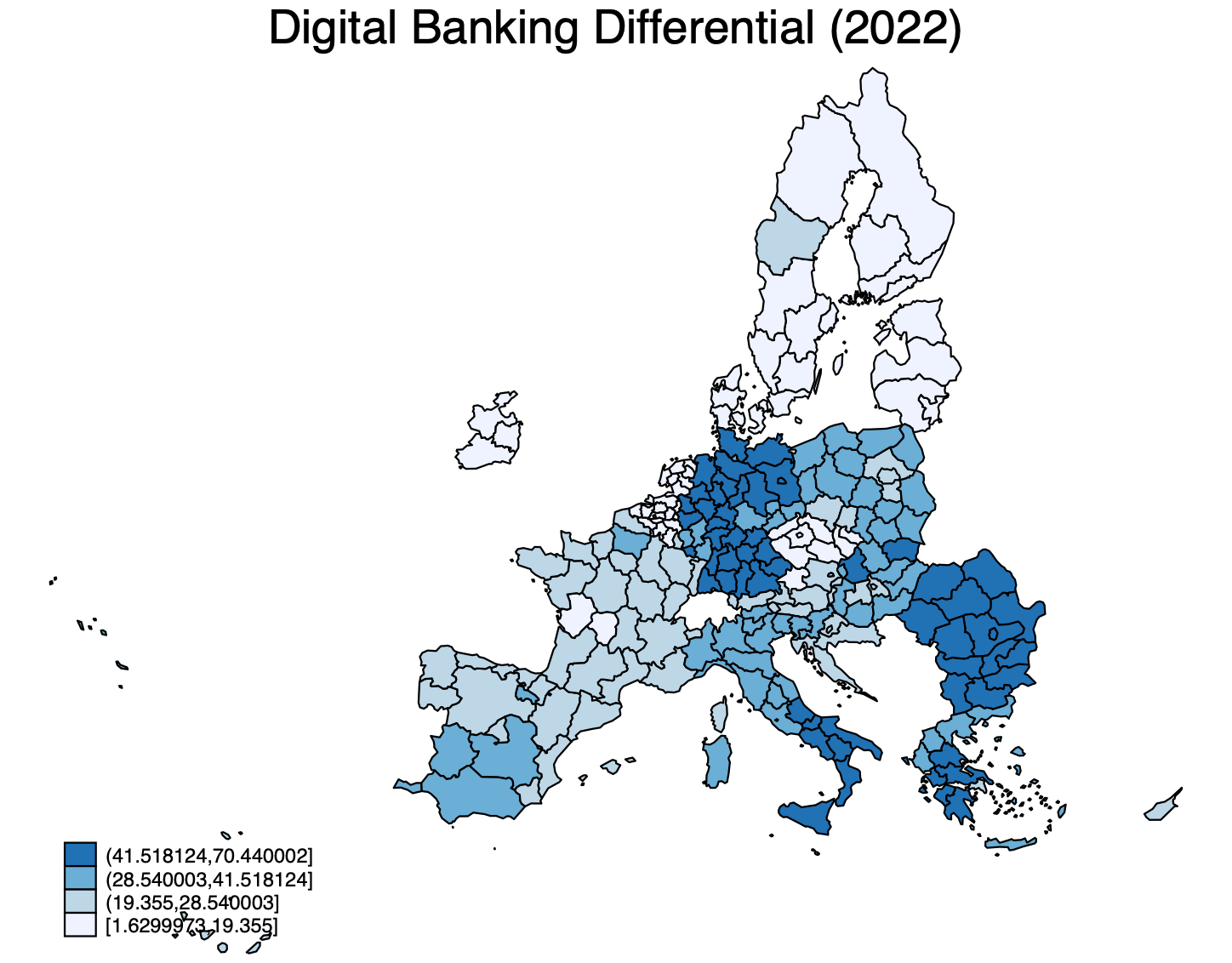

Measuring the Digital Banking Gap

The outcome variable is the Digital Banking Differential (DBD), defined as the difference between the share of individuals using the internet for private purposes and the share using internet banking within a region:

DBD_{it} = InternetUse_{it} – InternetBanking_{it}

This measure isolates the adoption decision among those with digital access. Rather than capturing overall usage levels, the DBD focuses on internet users who abstain from digital banking despite having access. This aligns directly with the Technology Acceptance Model, which is designed to explain adoption behavior rather than infrastructure availability.

Using raw digital banking usage rates would conflate adoption with access. By conditioning on internet use, the DBD captures latent resistance to adoption, reflecting suppressed perceived usefulness, perceived risk, or other behavioral frictions emphasized by TAM. While the average DBD across the EU has declined over time, dispersion across regions has increased. In some regions, up to 80 percent of internet users do not use digital banking, underscoring persistent regional differences in adoption behavior.

Empirical Strategy and Hypotheses

Because transposition into national law was mandatory under threat of fines and economic exclusion, all 27 EU member states implemented PSD2 between 2015 and 2020. As a result, there is no never-treated group. This makes a standard difference in differences design inappropriate, as it relies on untreated units to form a counterfactual.

Instead, the analysis uses a staggered difference in differences framework that exploits variation in the timing of implementation across countries and regions. Regions that have not yet implemented PSD2 serve as comparison units for those already treated. This approach allows estimation of the average treatment effect on treated regions under the assumption that treated and not-yet-treated regions follow comparable trends prior to implementation.

A negative and statistically significant post-implementation effect, combined with evidence of parallel pre-treatment trends, is interpreted as evidence that PSD2 reduced the Digital Banking Differential. This directly tests Hypothesis 1, namely that a policy-induced increase in perceived usefulness leads to higher adoption of digital banking among internet users.

Implementation timing is obtained from publicly available EUR-Lex records. For each country, the treatment year is defined as the first year in which PSD2 legislation is formally referenced under Directive 2015/2366. This yields four adoption cohorts: countries implementing in 2017, 2018, 2019, and 2020.

Most implementation occurred in 2018, when nearly three-quarters of EU member states and roughly 60 percent of regional observations transposed PSD2 into national law. Earlier adoption was limited to a small number of countries, while a handful implemented later. This distribution provides sufficient variation in treatment timing while preserving meaningful pre-treatment periods for most regions.

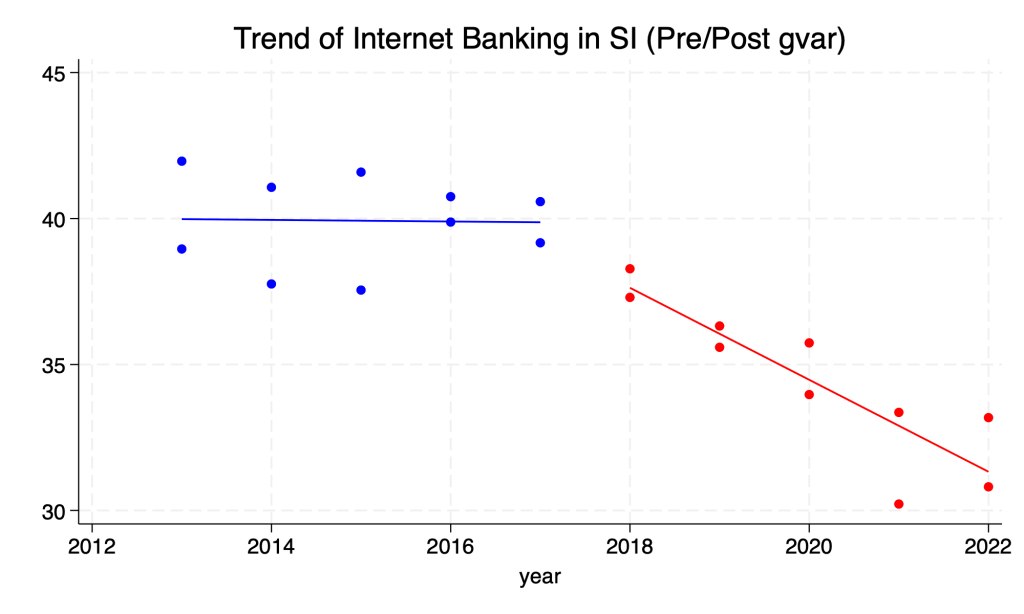

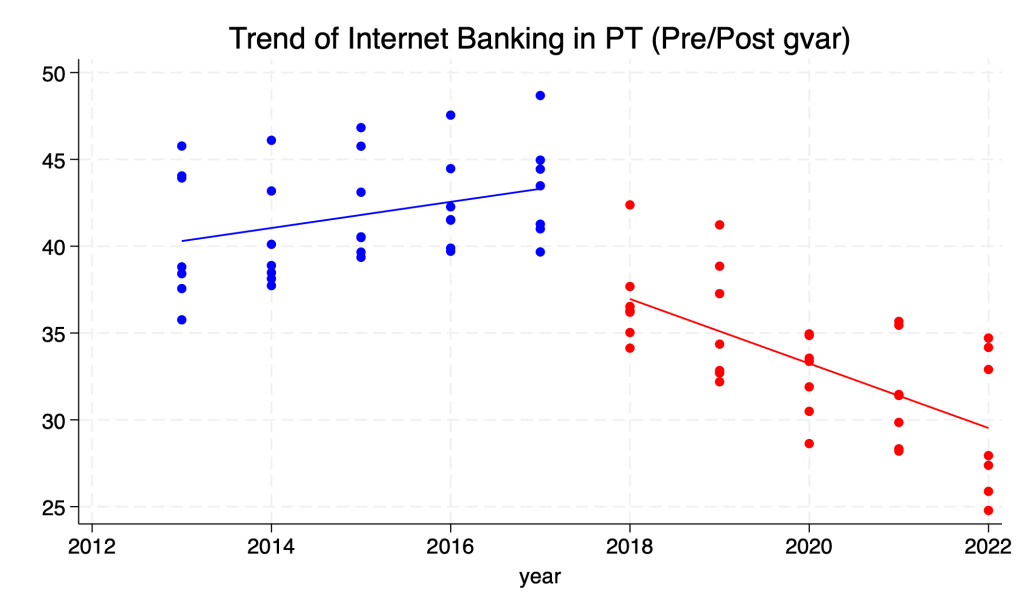

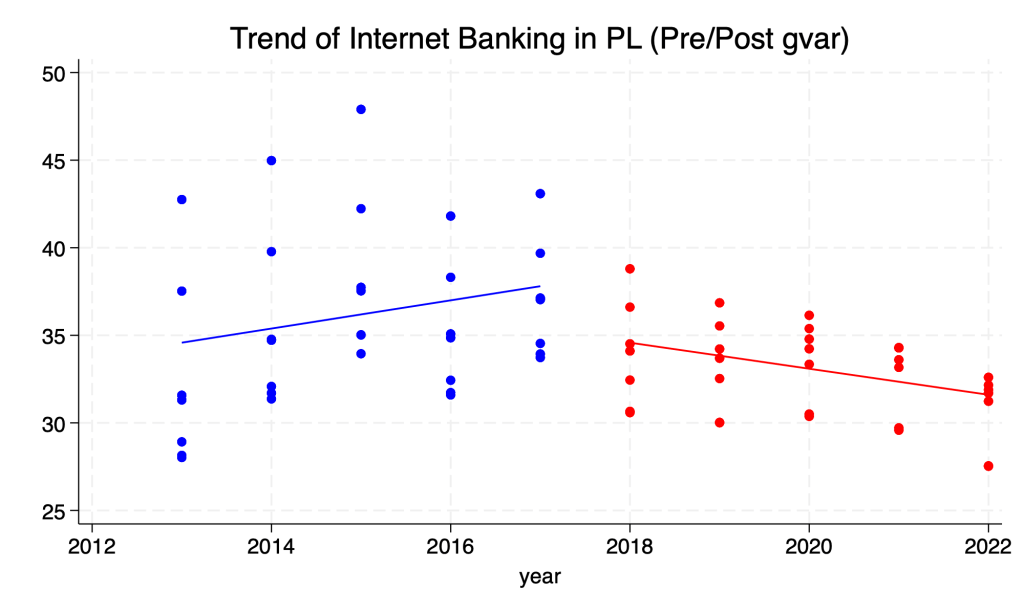

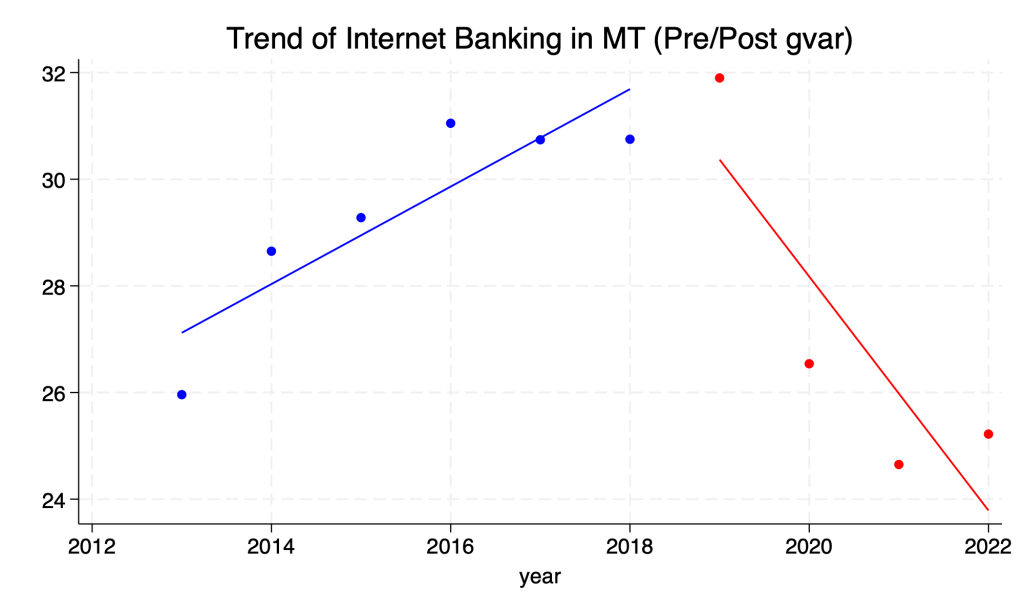

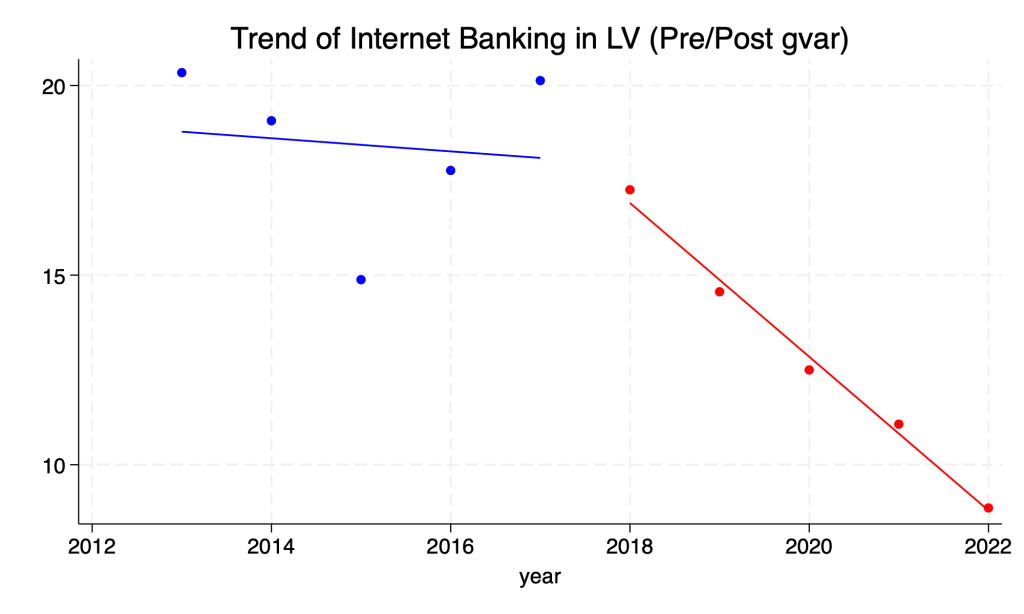

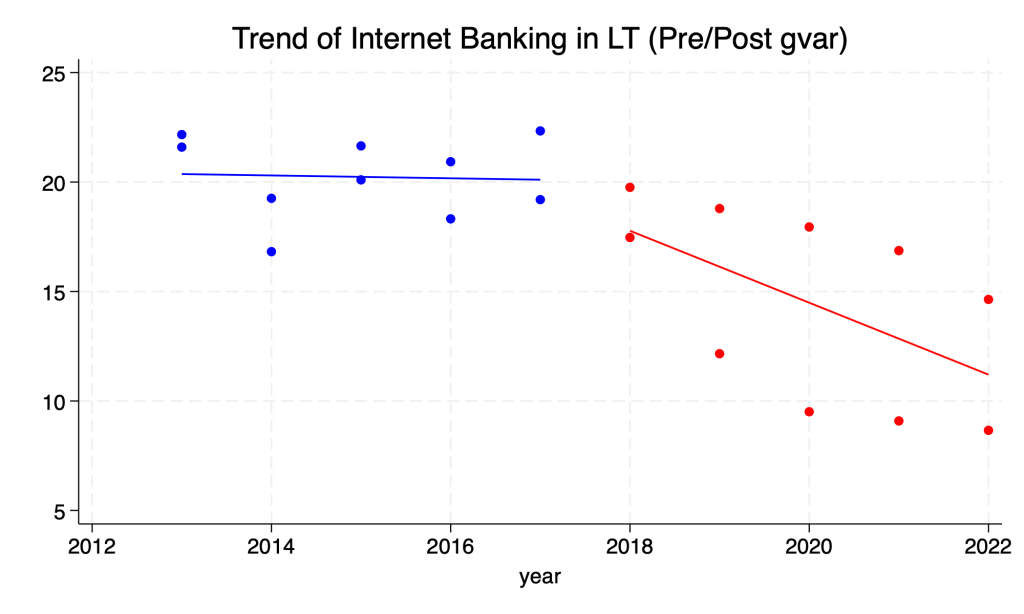

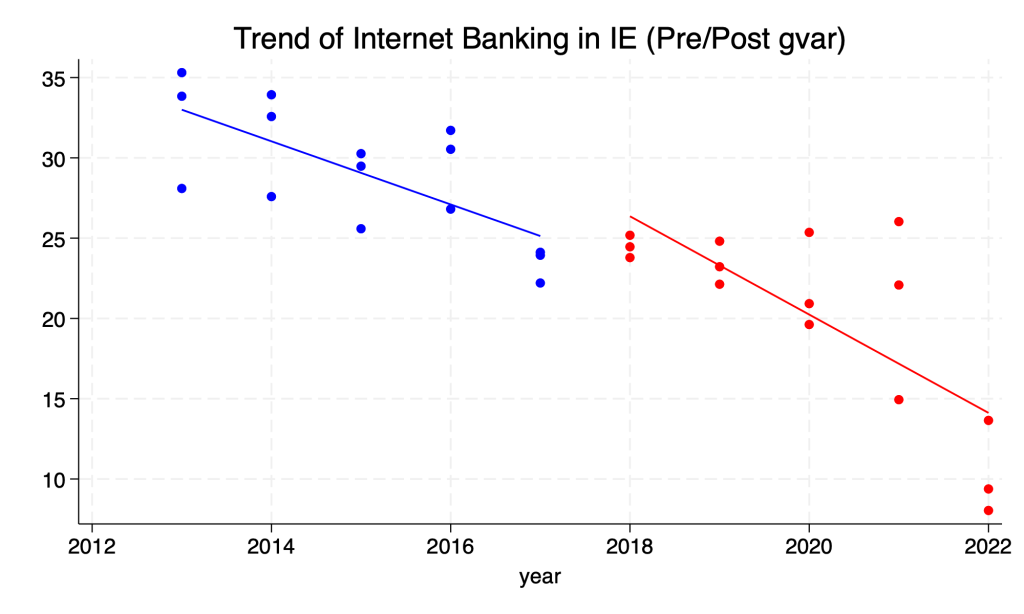

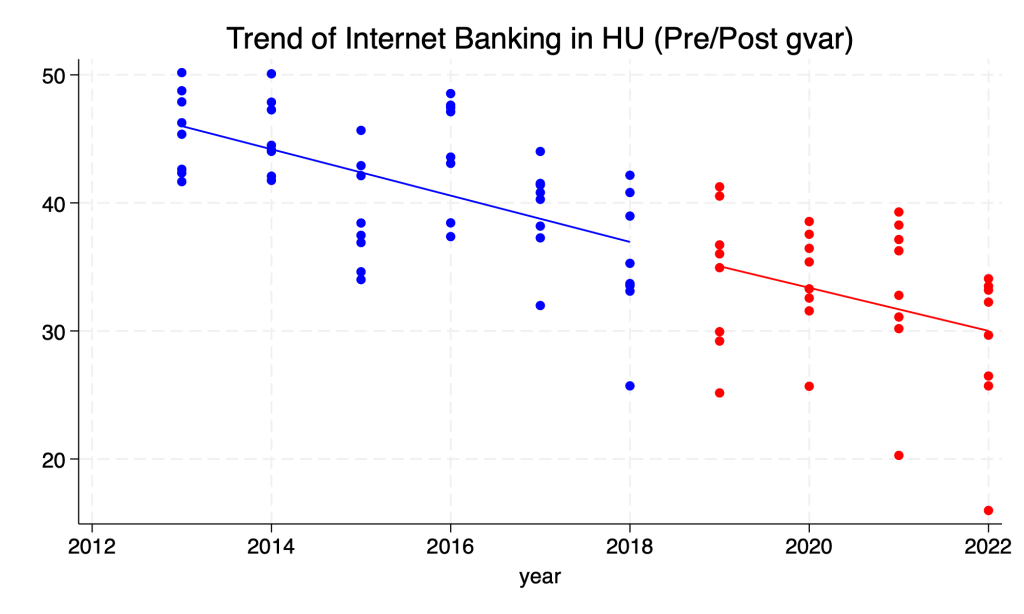

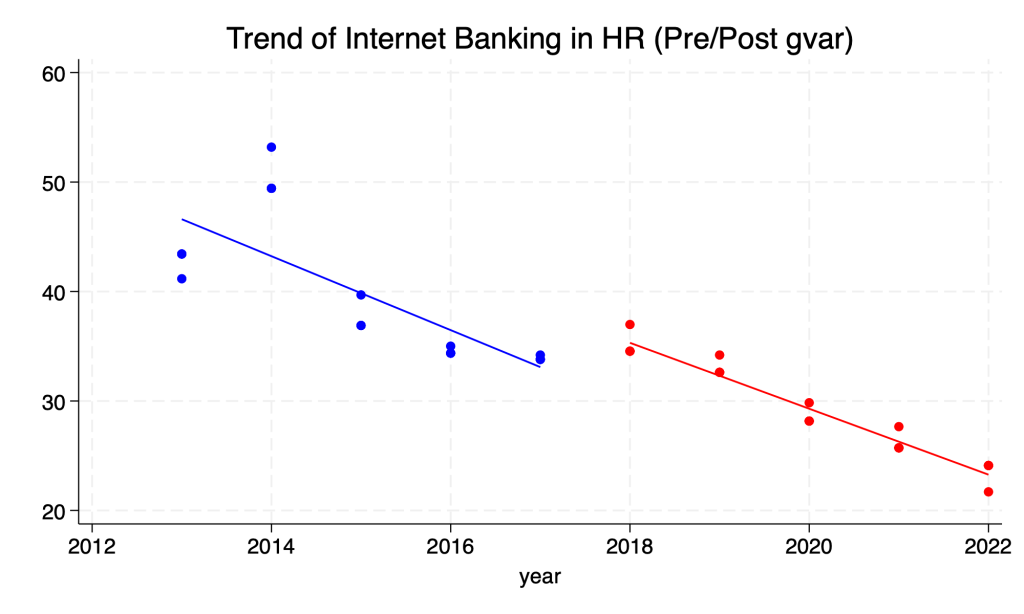

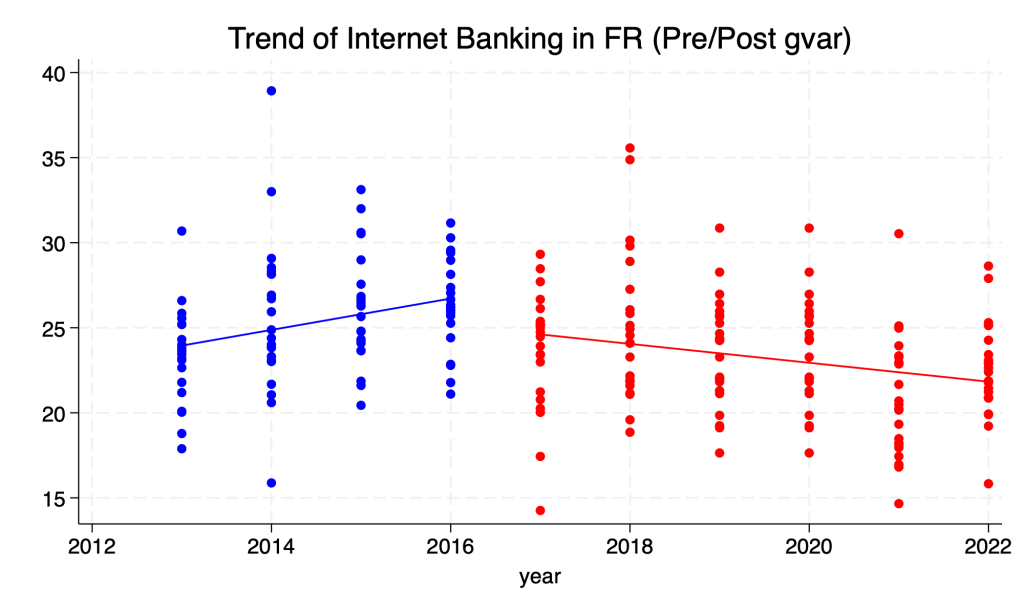

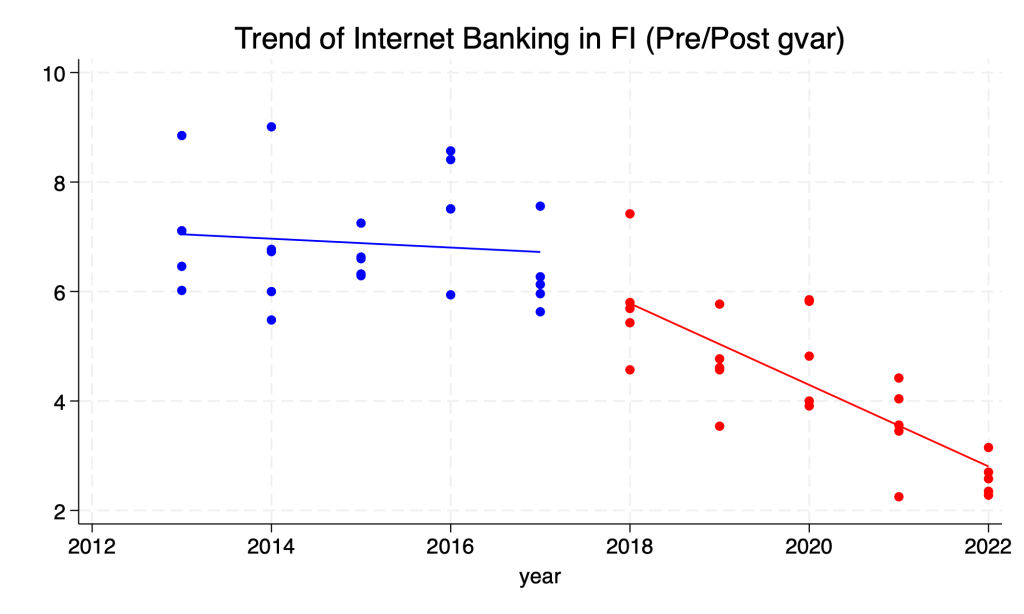

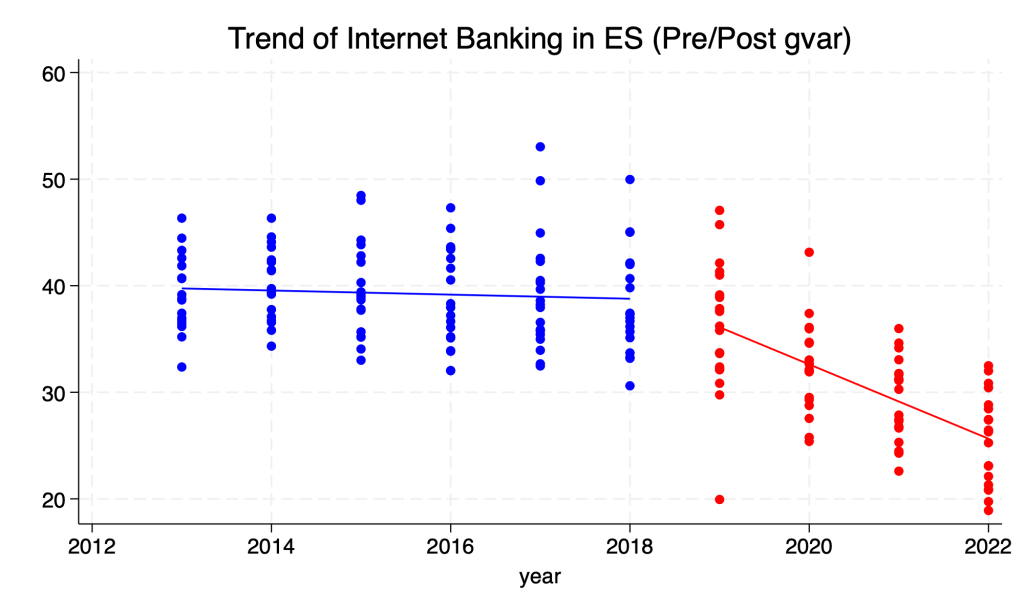

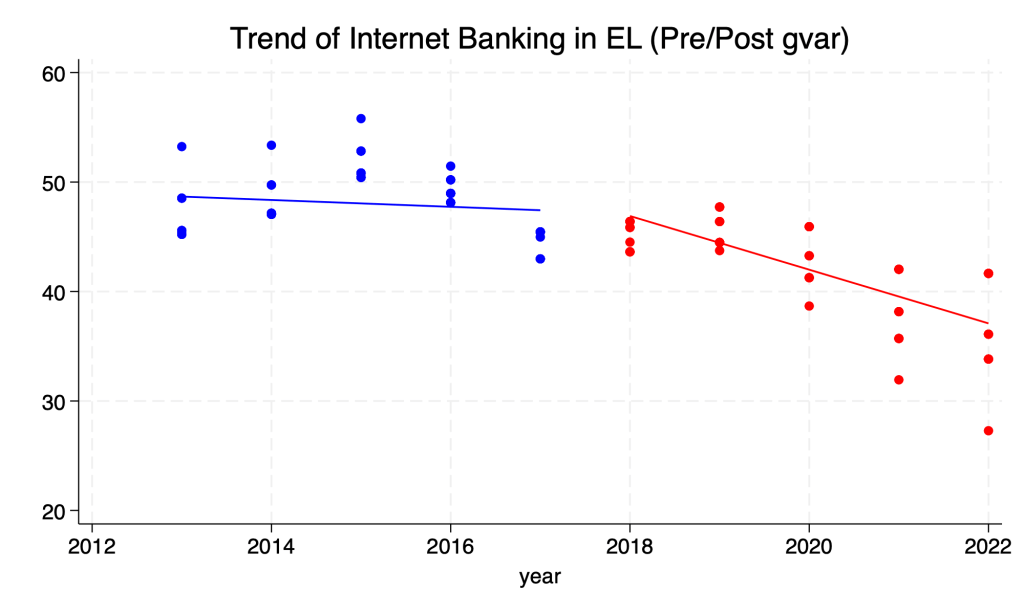

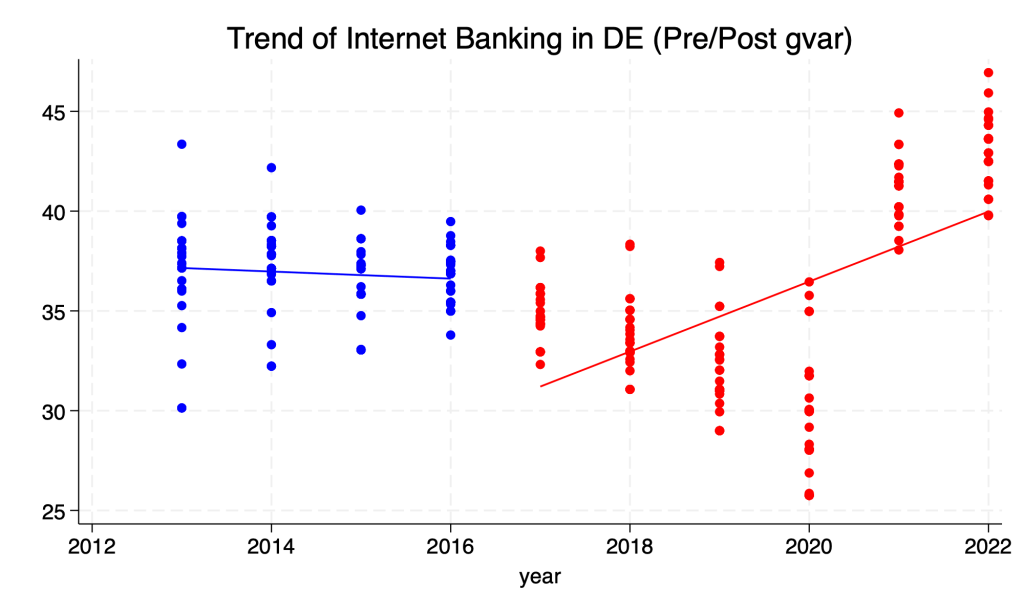

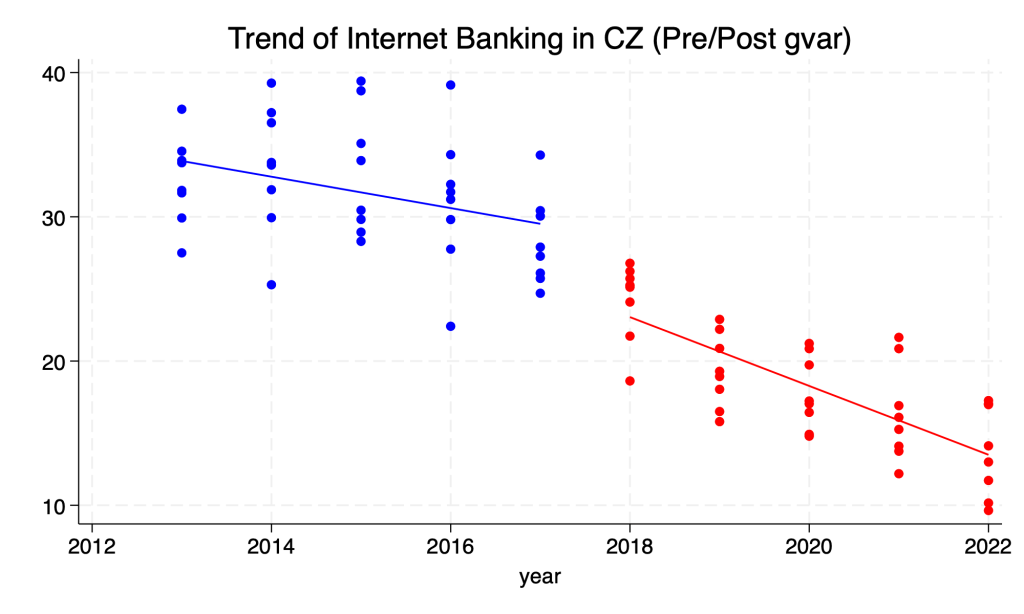

Preliminary visual inspection of regional trends suggests that the Digital Banking Differential declines following PSD2 implementation in many countries. While these patterns are not causal evidence, they are consistent with the hypothesized mechanism and motivate the formal estimation. The persistence of post-implementation declines further suggests that the policy effect may strengthen over time as users internalize improvements in security, trust, and consumer protection.

This framework provides a policy-based test of whether increasing perceived usefulness translates into measurable changes in digital banking adoption behavior.

Causal Interpretation Condition: Pre-treatment Trends

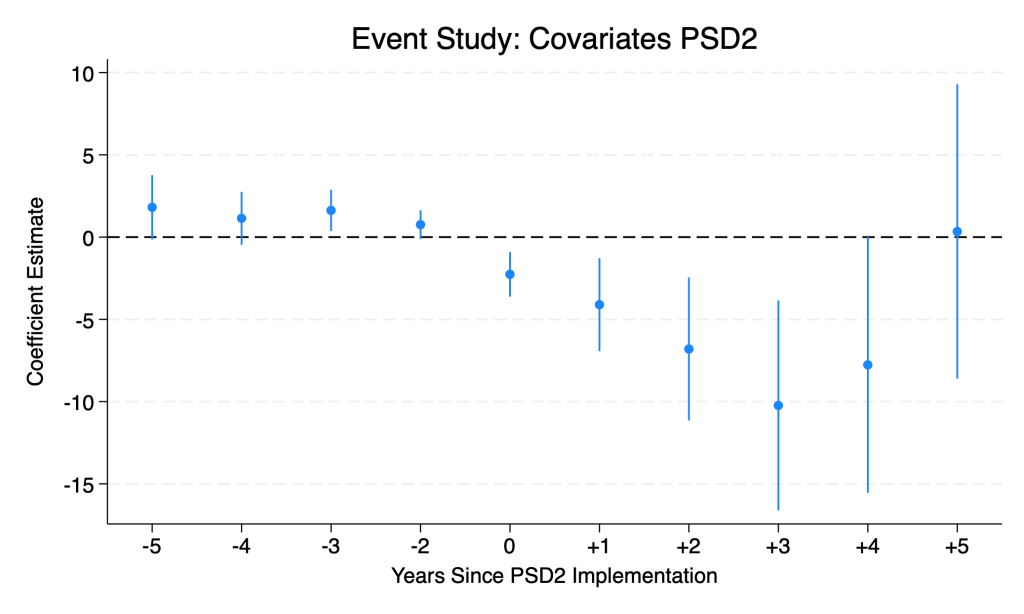

Credible difference in differences estimates require parallel pre-treatment trends. Because this analysis uses not-yet-treated regions as comparators, this assumption is especially fragile. I assess it using an event study that estimates year-by-year effects relative to the year before implementation.

In baseline specifications, several pre-treatment coefficients are statistically different from zero and positive, turning negative only at implementation. This pattern suggests possible anticipation effects and weakens the credibility of the counterfactual. Adding controls for economic conditions (as can be seen in the event study below), population, institutional quality, and fixed effects largely attenuates these differences, though minor deviations remain.

Post-treatment coefficients are consistently negative and increase in magnitude over time, indicating a dynamic effect that strengthens as PSD2 implementation diffuses and behavioral responses adjust.

PSD2 imposed a uniform regulatory framework across member states, supporting a consistent treatment definition. Institutional quality controls help account for differences in enforcement capacity, and spillovers are likely limited due to nationally bounded regulation.

Overall, the results are consistent with PSD2 reducing the digital banking differential, but violations of pre-treatment assumptions may require cautious interpretation.

Estimation

Because all EU-27 member states implemented PSD2 within a short time window, there is no never-treated group. This rules out comparisons with untreated units, including non-EU European countries that adopted similar technical standards. The analysis therefore relies on variation in implementation timing across countries and regions.

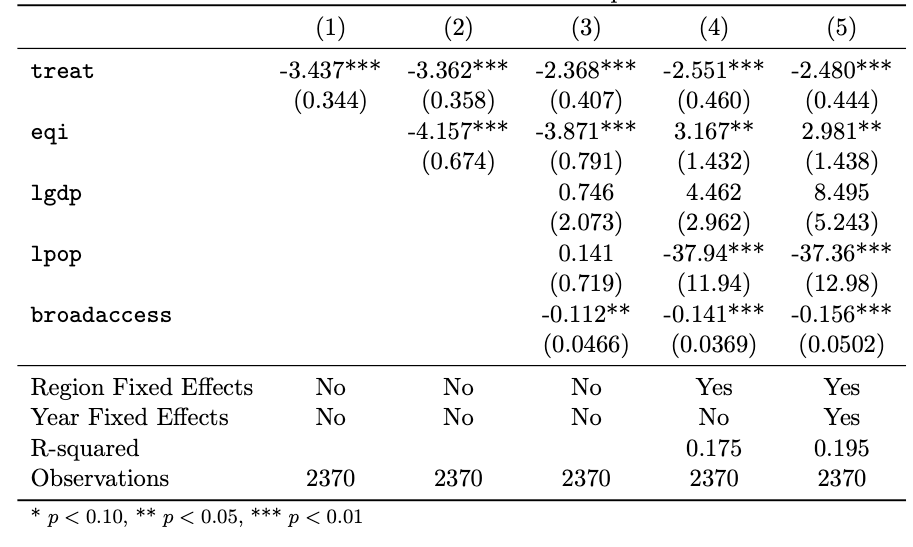

I begin with a two-way fixed effects (TWFE) specification, where treatment is defined as an indicator equal to one in all years following PSD2 implementation. The model controls for region and year fixed effects, as well as time-varying regional characteristics. The estimated coefficient captures the average change in the Digital Banking Differential following implementation.

Across all specifications, the PSD2 treatment effect is negative and statistically significant at the one-percent level. The magnitude is stable as controls are added. In the preferred specification, PSD2 is associated with an average reduction of roughly 2.5 percentage points in the Digital Banking Differential, indicating increased adoption of digital banking among existing internet users. This finding is consistent with Hypothesis 1.

However, TWFE assumes homogeneous treatment effects and uses already-treated regions as controls, both of which are problematic in settings with staggered adoption and dynamic responses. To address this, I re-estimate the effect using a staggered difference in differences framework that compares treated regions only to not-yet-treated ones.

Under this approach, the estimated average treatment effect is larger in magnitude. Regions exposed to PSD2 experienced an average reduction in the Digital Banking Differential of about 4 percentage points. Group-specific estimates show the strongest effects for the 2018 adoption cohort, which contains the majority of observations.

Despite consistent signs and magnitudes across specifications, formal tests indicate violations of parallel pre-treatment trends. As a result, these estimates should not be interpreted as definitive causal effects. Rather, they provide robust evidence of an association between PSD2 implementation and increased digital banking adoption.

Taken together, the results support the hypothesis that a policy-induced increase in perceived usefulness is linked to higher adoption among internet users. While causal interpretation requires caution, the consistency of the findings justifies further analysis of the underlying behavioral mechanisms emphasized by the Technology Acceptance Model.

Leave a comment